Specialty Drug Distribution Market Report OverviewSpecialty Drug Distribution Market size in 2019 is estimated to be $1.5 billion, growing at a CAGR of 11.5% during the forecast period 2020-2025. Specialty drugs are medications that are used to treat chronic diseases such as cancer, rheumatoid arthritis, and multiple sclerosis. Specialty drugs are high cost oral or injectable medications. It is high complex Medications that require specialized handling, distribution and temperature control. Increasing prevalence of chronic diseases coupled with rising demand of specialty drugs across the globe are the major factors driving the growth of the market. Moreover, better distribution facilities and rising advancement in healthcare further enhance the overall market demand for Specialty Drug Distribution during the forecast period 2020-2025.

Report Coverage

The report: “Specialty Drug Distribution Market – Forecast (2020-2025)”, by Industry ARC, covers an in-depth analysis of the following segments of the Specialty Drug Distribution Market:By Application : Oncology, AIDS, Multiple Sclerosis, Rheumatoid Arthritis, Hemophilia, OthersBy Distribution Channel : Full line Wholesalers, Specialty DistributorsBy End User : Independent Pharmacies, Large Chain Pharmacies, Hospitals & Clinics, Online Retailers By Geography : North America, Europe, Asia-Pacific, and Rest of the World

In 2019, North America dominates the Specialty Drug Distribution Market owing to increasing usage of specialty drugs for the treatment of chronic diseases.

Better healthcare reforms coupled with increased number of distribution facilities is driving the market growth of Specialty Drug Distribution.

Detailed analysis of the Strength, Weakness, and opportunities of the prominent players operating in the market will be provided in the Specialty Drug Distribution Market report.

Specialty Drug Distribution Market Segment Analysis – By Application

Based on the Application, Specialty Drug Distribution Market is segmented into Oncology, AIDS, Multiple Sclerosis, Rheumatoid Arthritis, Hemophilia, Others. The oncology segment is forecast to be the fastest-growing segment and is projected to grow at a CAGR of 9.8% during the forecast period 2020-2025. This is mainly owing to growing usage of specialty drugs for the treatment of cancer across the globe. According to World Health Organization (WHO), cancer is the second leading cause of death in world and in 2018, nearly 9.6 million people die because of cancer in globally.

Specialty Drug Distribution Market Segment Analysis – By Distribution Channel

Based on the distribution channel, Specialty Drug Distribution Market is segmented into Full line Wholesalers, Specialty Distributors. In 2019, Full line Wholesalers held the largest share in the Specialty Drug Distributions market. This is mainly owing to efficient and excellent supply chain and logistics. Moreover, Full line Wholesalers is fast and frequent delivery service is also contributing to the growth of this segment.

Specialty Drug Distribution Market Segment Analysis – Geography

North America dominated the Specialty Drug Distribution market share accounting for 40% of the market in 2019. This is mainly owing to increasing usage of specialty drug for the treatment of chronic diseases in this region. According to National Health Council, in America chronic diseases affect approximately 133 million Americans which increases the demand of Specialty Drug Distribution Market.However, the Asia-Pacific region is projected to be the fastest-growing during the forecast period 2020-2025. This is owing to innovative distribution channel coupled with advancement in healthcare.

Increasing usage of specialty drug for the treatment of chronic diseases such cancer, rheumatoid arthritis, and multiple sclerosis are some factors driving the growth of Specialty Drug Distribution market.

Better logistics facilities

Better logistics facilities coupled with efficient supply chain some factors driving the growth of the market. Also, innovative distribution facilities further contributing to the growth of Specialty Drug Distribution Market.

Specialty Drug Distribution Market Challenges

Restriction on distribution channel is challenging the growth of the market as brand manufacturers are using this to reduce generic competition by preventing generic companies from getting samples brand product. Moreover, changing preference of consumer inorder to get the product at low price and bypass distribution channels are further restraining its market growth during the forecast period 2020-2025.

Specialty Drug Distribution Industry Outlook

Product launches, Merger & Acquisitions, joint ventures and R&D activities are key strategies adopted by players in the Specialty Drug Distribution Market. Specialty Drug Distribution top 10 companies are Smith Drug Company, Pfizer Inc., Anda Distribution, Rochester Drug Cooperative, Cardinal Health, Mckesson Corporation, H.D. Smith, Grainger, Amerisource Bergen, and Cintas. Buy Now

Acquisitions/Product Launches:

In June 2018, McKesson Corporation has acquired Medical Specialties Distributors, LLC, a leading supply chain provider of medical supplies, biomedical services, and technology solutions.

In September 2015, Grainger has acquired Cromwell Group Limited, the largest independent MRO distributor in the United Kingdom. This acquisition helps to accelerated growth and scale for Grainger’s online MRO model in the U.K. and Germany.

For more Lifesciences and Healthcare related reports, please click here

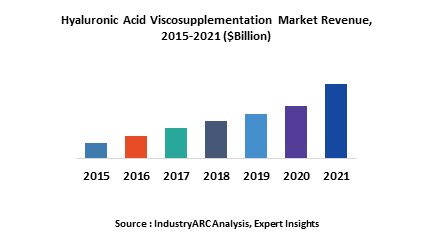

Hyaluronic Acid Viscosupplementation Market OverviewViscosupplementation is one of the treatment procedures to relieve Osteoarthritis. Hyaluronic acid is found in synovial fluids surrounding the joints. It acts as a lubricating agent, enabling smooth movement of the bones. The Hyaluronic Acid Viscosupplementation market is segmented based on the course of treatment, which is again sub-segmented based on the different doses of injections. The market is also categorized based on anatomy and end user. The Hyaluronic Acid Viscosupplementation market is estimated to grow at a CAGR of 6.36% through 2023. Hyaluronic Acid Viscosupplementation Market Outlook Hyaluronic Acid Viscosupplementation helps in improving the mobility of the joints and improves the comfort level during any activity. On the basis of course of treatment, the single injection segment dominates the market and is estimated to grow at a CAGR of 7.71% through 2023. Based on anatomy, the Knee segment is projected to grow at the highest CAGR during the forecast period. The North America Hyaluronic Acid Viscosupplementation market is forecast to grow at a CAGR of 6.56% through 2023. However, Asia-Pacific is estimated to dominate the market during the forecast period due to the rising elderly population.

Hyaluronic Acid Viscosupplementation Market Growth Drivers The Hyaluronic Acid Viscosupplementation Market is largely driven by the growing awareness among patients about the new treatments of osteoarthritis. Rising prevalence and incidence of osteoarthritis is accelerating the growth of the market. Rising obese population globally and increasing geriatric population are also major factors for the growth of the market. Growing awareness about the benefits of minimally invasive surgical procedures for osteoarthritis is one of the key factors that drive the hyaluronic acid viscosupplement market’s growth. Hyaluronic Acid Viscosupplementation Market Challenges Lack of safety and efficacy associated with viscosupplementation products pose major challenges for the market. Complex Regulatory processes regarding the products of Viscosupplementation may slow down the market because it takes a long time to get approval for any product from the regulatory bodies. The reimbursement policies associated with the treatment varies from one country to another, and thus, this can also pose challenges for the market.

Hyaluronic Acid Viscosupplementation Market Research Scope:-The base year of the study is 2017, with forecast done up to 2023. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on volume shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the Hyaluronic Acid Viscosupplementation market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of treatment, by anatomy and vaccines by disease indication. Hyaluronic Acid Viscosupplementation Market Report: Industry Coverage By Course of Treatment: Single Injections, Multiple Injections By Anatomy: Knee Osteoarthritis, Hip Osteoarthritis, Ankle Osteoarthritis, and Shoulder Osteoarthritis. By End User: Hospitals, Clinics and Ambulatory Surgical Centers. The Hyaluronic Acid Viscosupplementation Market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: The U.S, Canada, Mexico

Europe: The U.K, Germany, France, Italy, Spain, Rest of Europe.

APAC: China, Japan, South Korea, India, Rest of APAC.

Rest of World (RoW): South America, the Middle East and Africa.

Hyaluronic Acid Viscosupplementation Market Key Players Perspective: Labrha International launched HAPPYMINI for the treatment of Temporo-Mandibular Osteoarthritis. Labrha provides a complete range of new and innovative viscosupplement. Some of the other key players in this market are LG Chem Ltd, Bioventus Inc., Sanofi Genzyme, Anika Therapeutics, Seikagaku Corporation and many others. Hyaluronic Acid Viscosupplementation Market Trends

Product Launch was the dominant strategy adopted by the prominent players of Hyaluronic Acid Viscosupplementation Market, crediting up to 50% of the share of the total market, followed by acquisition.

Bioventus Inc launched OSTEOAMP SELECT Fibers, which is an innovative addition to its allograft line of OSTEOAMP bone graft substitutes.

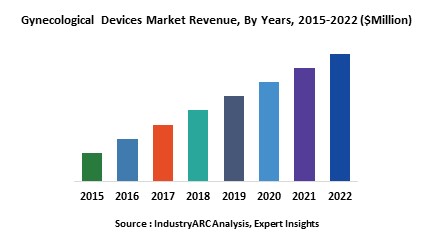

The Gynaecological devices Market is $10,592.81million in 2017 and is estimated to surpass $13,484.50 million mark during 2018-2023 growing at an estimated CAGR of more than 5.05%. By region north-America dominated the overall Gynaecological market. Laparoscopes dominated the overall gynecological device market with a share of 40% and generated a revenue of 629.34m in 2017 and is estimated to grow at a CAGR of 4.33% to reach $773.90 during 2018-2023.What are Gynaecological devices?Gynaecological devices are available with coated and un-coated stainless steel options and are designed to deliver physicians with greater efficiency and their patients with maximum efforts. Gynaecological devices are extensively used in hospitals, clinics/ASC, research institutes and diagnostic labs for surgical and examination purposes. Various gynecological devices include such as fluid management devices, pelvic floor electrical stimulation devices, gynaecological forceps, gynaecological curettes, endometrial ablation devices, pelvic organ prolapse repair device.

What are the major applications for Gynaecological devices?

The major end users of Gynaecological devices are hospitals, clinics, research institutes, diagnostic labs for surgical and examination purposes.

Market Research and Market Trends of Gynaecological devices

In 2018, RAIING Medical invented a device named IFertracker, a wearable thermometer that can be attached directly to the user body to continuously measure core body temperature every night during sleep. Simultaneously IFertracker also calculates and charts the user’s Basal body temperature and predicts her fertile window, ultimately offering a fertility tracking method that helps users learn more about their bodies and get pregnant faster.

Flexible ultrasound transducer have been developed to provide 3D views of objects beneath. These are flexible and can be used on curvy surfaces such as knees, stomach, moving substances etc. this product featured of 100 piezoelectric transducers which are arranged in a square array connected to each other. In healthcare this help doctors diagnose variety of conditions in humans.

OmniGuide, based in Lexington, MA, is releasing new laparoscopic shears, These FMsealer Laparoscopic Shears, do not release electric current into the tissues when transecting and sealing and a lot less heat is transferred to nearby tissues. It is safe to use and reduce risk of capacitive coupling.

Willow, introduced a sleek wearable breast pump to collect breast milk without the help of any wires or external components. The milk is collected in a specially designed bag that is fitted inside the unit. This bag can be easily removed to transfer the milk. The device is rechargeable and also have an accompanying cellphone app.

Increasing adoption of robotic navigation technologies for laproscopy can be considered as the greatest surgical innovations as it is well known for minimal invasive procedures leads to faster recovery, decreased blood loss, shorter hospital stay.

Who are the Major Players in Gynaecological devices market?

The companies referred in the market research report includes Johnson & Johnson, General Electric Co, Siemens AG, Medtronic Inc, Baxter international, Covidien Plc, Koninklijke Philips Electronics NV, Fresenius Medical Care AG & Co. KGAA, Olympus corporation.

What is our report scope?

The report incorporates in-depth assessment of the competitive landscape, product market sizing, product benchmarking, market trends, product developments, financial analysis, strategic analysis and so on to gauge the impact forces and potential opportunities of the market. Apart from this the report also includes a study of major developments in the market such as product launches, agreements, acquisitions, collaborations, mergers and so on to comprehend the prevailing market dynamics at present and its impact during the forecast period 2018-2024. All our reports are customizable to your company needs to a certain extent, we do provide 20 free consulting hours along with purchase of each report, and this will allow you to request any additional data to customize the report to your needs.

Evaluate market potential through analyzing growth rates (CAGR %), Volume (Units) and Value ($M) data given at country level – for product types, end use applications and by different industry verticals.

Understand the different dynamics influencing the market – key driving factors, challenges and hidden opportunities.

Get in-depth insights on your competitor performance – market shares, strategies, financial benchmarking, product benchmarking, SWOT and more.

Analyze the sales and distribution channels across key geographies to improve top-line revenues.

Understand the industry supply chain with a deep-dive on the value augmentation at each step, in order to optimize value and bring efficiencies in your processes.

Get a quick outlook on the market entropy – M&A’s, deals, partnerships, product launches of all key players for the past 4 years.

Evaluate the supply-demand gaps, import-export statistics and regulatory landscape for more than top 20 countries globally for the market.

For more Lifesciences and Healthcare related reports, please click here

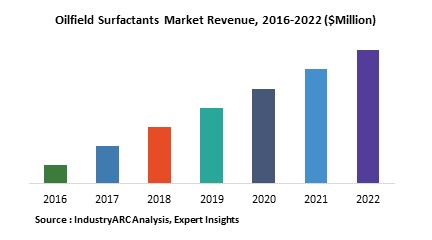

Oilfield Surfactants Market Overview:The global market for Oilfield Surfactants was estimated at $798.37 million in 2016 and is predicted to witness robust and accelerated growth in the coming years, especially in the oil producing countries such the US, China and members of the OPEC. Demand for oilfield surfactants has grown since the need for chemicals in sustainable oil exploration, extraction and production has skyrocketed as witnessed in the rigorous EOR (Enhanced Oil Recovery) activities. Furthermore, there has been a growing interest in the bio-based oil surfactants, although being a niche market, for its environment friendly effects that can counter-act the wide environmental concerns about the oil and gas industries. Oilfield Surfactants Market Outlook:Oilfield surfactants are chemicals that effectively lower the surface tension between a fluid and a solid or between various fluids. Oilfield surfactants have various physical and chemical properties that can be exploited in the stages of drilling, production, refining, enhanced oil recovery and stimulation. Its applications vary from asphaltene dispersants, corrosion inhibition, emulsifiers, demulsifier intermediates, oil-wetters, paraffin inhibitors, water-wetters, foamers and defoamers. The type of surfactant behavior is dictated by the chemical structure, specifically the structural groups on the molecule). The oilfield surfactant market is segmented based on the stage of application such as drilling, production and stimulation as well as its applications as mentioned above.

Oilfield Surfactants Market Growth drivers:Global oil and natural gas production has been increasing steadily since the last decade with oil production recording 92.6 million barrels per day (BPD) with US being the largest oil producing country in the world. These statistics imply that as oil production, extraction and exploration activities increase, there is clearly a huge growth potential for oilfield surfactants to meet this large demand capacity. Surfactants such as emulsifiers, demulsifiers, biocides etc. would highly in demand at various stages of drilling, production and stimulation in oilfields. In addition, as the world plans to move towards a more sustainable and environment friendly future, bio-based oilfield surfactants would be in high demand. Enhanced Oil Recovery (EOR) is gaining increasing popularity in the oil industry as it cuts costs and maximizes yield, and thus this could clearly boost the Oil Surfactants market as EOR is only possible due to the usage of such surfactants. Oilfield Surfactants Market Challenges:The prime challenge faced by the Oilfield Surfactants market is the dangerous carbon footprint that the oil and gas industries leave behind in the world’s atmosphere. The use of fossil fuels has always been criticized and many developed countries in the EU planning to phase out their energy dependence on oil and natural gas. Growing environmental concerns about oilfield production levels coupled with massive oil spills are the major challenges to the Oilfield Surfactant market.

Oilfield Surfactants Market Research Scope:The base year of the study is 2017, with forecast done up to 2023. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on unit shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the Oilfield Surfactants market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of plastics in the Oilfield Surfactants market, and their specific applications in different types of vehicles.

Oilfield Surfactants Market Report: Industry Coverage Oilfield Surfactants–By Class of Substrate: Synthetic and Bio-based Oilfield Surfactants– By Application: Drilling, Stimulation and Stimulation Oilfield Surfactants– By Surfactant Class: Non-Ionic, Anionic, Cationic, Polymeric, Amphoteric and others The Oilfield Surfactants market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: The U.S., Canada, Mexico

South America: Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, Costa Rica

Europe: The U.K., Germany, Italy, France, The Netherlands, Belgium, Spain, Denmark

APAC: China, Japan, Australia, South Korea, India, Taiwan, Malaysia, Hong Kong

Middle East and Africa: Israel, South Africa, Saudi Arabia

Oilfield Surfactants Market Key Players Perspective:Some of the Key players in this market that have been studied for this report include: CP Kelco Oil Field Group, Huntsman Corporation, Croda International PLC, Weatherford International, Stepan Company, Enviro Fluid, Rimpro-India, Evonik Industries AG, Flotek Industries and others Buy Now Market Research and Market Trends of Oilfield Surfactants Market

Researchers at the University of Houston discovered an innovative technique using nanotechnology to maximize oil recovery from oil wells, as oilfields yield only 30-35% on average. The researchers have developed a graphene amphilic nanosheet designed from Janus nanoparticles that could aid in tertiary oil recovery. If producers can unlock this untapped potential, the crude oil supply could be boosted and could drive the selling price lower.

According to the 2018 BP Statistical Review of World Energy global oil production hit a record of 92.6 million barrels per day (BPD). This large increase in oil production levels would indicate a large demand for oilfield surfactants in the oil and gas industries.

Based in Texas, U.S, Huntsman Corporation is a global key player with a significant market share in the oilfield surfactant market. Huntsman Corporation recently acquired Nanocomp Technologies Inc., a company specialized in manufacturing advanced carbon materials based in New Hampshire, USA. Its popular product is an advanced carbon-based material branded as Miralon, which could have potential use in corrosion inhibition and can lead to a new class of nanomaterial based oilfield surfactant.

The location intelligence and location analytics is tipped to play a vital role in the coming years. By 2020, it is estimated that the number of connected devices are likely to reach 20.4 billion, a 2.5 times increase in devices from 2017. From computers to mobile phones, appliances to street signs, these so called connected devices (dubbed as Internet of Things) transmit huge amounts of data about what we do, where are we located, when do we use these devices and for what purpose. Location analytics tools are defining how companies are using geo spatial data to derive meaningful insight to address a particular problem. The transportation and logistics sector is expected to bring in majority of the revenue at present and expected to remain the same in coming years.What is Location Intelligence and Location Analytics?Location intelligence and location analytics use a combination of business intelligence and geo spatial data to derive meaningful insights for business outcomes through data enrichment, visualization and iterative analysis. Location data consists of a wide range of data relating to longitudes, latitudes, altitudes, existing points, the direction of travel and a record of the users last location. Location analytics use the collected data with Business intelligence tools to assess, analyze and process the data collected into actionable information and enable effective business outcomes.

Market Research and Market Trends of Dark Analytics Market

Many industry experts consider Location Analytics to be used extensively for the entire length and breadth of the industry in coming years. Industry leaders in retail are installing sensors, Bluetooth beacons and WIFI routers to connected customers devices to gather information. Using location intelligence and analytics organizations track consumer data such as in store foot map, products stashed on online baskets, a record of their purchases and trends on social media. Rise in penetration of mobile phones and connected devices retailers are able to gather actionable information for future insights.

Transportation and logistics are major industries who are set to benefit the most from this technology. Companies like Uber rely on location technology to detect traffic patterns, show an approximate waiting time, and map the short way possible and an estimated fare. Uber partnered with factual, a geo data specialist to enhance its navigation technologies for their self-driving cars.

Grocery stores such as Amazon and Kroger Co. employ advanced analytics using IOT to keep a track of their customer’s choices and products based on their regularity. Using this data enterprises provide tailor made product deals, merchandising, marketing and even product development strategies.

Who are the Major Players in Location Intelligence & Location Analytics Market?The major vendors in the Location Intelligence & Location Analytics market are IBM Corporation, Cisco Systems Inc., Oracle Corporation, TIBCO Software Inc., Galigeo SAS, Pitney Bowes Inc., SAS Institute Inc., and Google Inc. among others. What is our report scope?The report incorporates in-depth assessment of the competitive landscape, product market sizing, product benchmarking, market trends, product developments, financial analysis, strategic analysis and so on to gauge the impact forces and potential opportunities of the market. Apart from this the report also includes a study of major developments in the market such as product launches, agreements, acquisitions, collaborations, mergers and so on to comprehend the prevailing market dynamics at present and its impact during the forecast period 2018-2023. All our reports are customizable to your company needs to a certain extent, we do provide 20 free consulting hours along with purchase of each report, and this will allow you to request any additional data to customize the report to your needs.

Evaluate market potential through analyzing growth rates (CAGR %), Volume (Units) and Value ($M) data given at country level – for product types, end use applications and by different industry verticals.

Understand the different dynamics influencing the market – key driving factors, challenges and hidden opportunities.

Get in-depth insights on your competitor performance – market shares, strategies, financial benchmarking, product benchmarking, SWOT and more.

Analyze the sales and distribution channels across key geographies to improve top-line revenues.

Understand the industry supply chain with a deep-dive on the value augmentation at each step, in order to optimize value and bring efficiencies in your processes.

Get a quick outlook on the market entropy – M&A’s, deals, partnerships, product launches of all key players for the past 4 years.

Evaluate the supply-demand gaps, import-export statistics and regulatory landscape for more than top 20 countries globally for the market.

Fiber cement is a popular building material that gives best benefits in the siding industry longevity. It is a composite of sand, portland cement, and cellulose fibers are one of the sustainable materials. These helps to withstand at the harsh weather compared to other materials. The Global Fiber Cement market generated revenue of $13350.26 million in 2017 and is projected to grow at a CAGR of 4.86% during the forecast period 2018-2023. Asia pacific region is the major fiber cement market share holder with more than 35% in the global fiber cement market. The presence of numerous raw material suppliers is expected to continue its growth in fiber cement market size in construction sector. Fiber Cement Market Industry analysis states residential application is the dominant segment valued $4955.62 million in 2017 and is estimated to grow at a CAGR of 4.6% during the forecast period 2018-2023. Fiber cement board made of cement, silica sand, and special cellulose fiber, and selected filler is an autoclave reinforced fiber cement board used in residential and commercial activities at a large scale, thereby driving the fiber cement market during the forecast period.

Fiber cement is a synthesized in building and construction material, mainly used in roofing and facade products due of its strength and durability. Growing advantage of easy installation of fiber cement siding on buildings has made familiar in the market. Fiber cement siding is a building material used to cover the exterior of a building in both commercial and domestic applications. Fiber cement is a composite material made of cellulose material and cement fortified. Originally, Asbestos was used as the supporting material but due to safety concerns, that was replaced by cellulose. Fiber cement siding has several advantages since it is resistant to termites, impact resistant, does not rot, and has fire resistant properties. The product has various uses such as Internal cladding, External cladding, Roofing and others. Polypropylene is the leading fiber type in fiber cement market industry. It has a major application in injection molding. The fiber cement are processed using Hatschek process, Extrusion Process, and Pertile Process, among all extrusion process is commonly used in manufacturing of cement boards, and holds a share of 64% of the global fiber cement market share. The Hatsheck process was firstly developed for the making of asbestos composites, but it is now used for the manufacture of non-asbestos, cellulose fiber reinforced cement composites.

What are the major applications for Fiber Cement?

The various end users include Agriculture, Residential, Non-Residential, Industrial, Commercial and others. Various applications are Laminated Skirts, Internal cladding (Window sills, Partition walls, Fire protection, Ceilings and floors), External Cladding (Corrugated sheets, Planks, Shingle Slates, Building Facades, Flat sheets, Underroof), Roofing and others. Fiber cement market industry analysis predicts the growing advancement of chemical composition, and growing adoption, the threat from wood and vinyl siding is expected to compete in the upcoming market.

Market Research and Market Trends of Fiber Cement Ecosystem

The Austrian based company named Rieder Smart Elements GmbH, recently came up with a new infrastructure called Rieton, the track absorber, which consists of aerated concrete is installed between on the outsides of the firm railway tracks. In contrast to other noise protection systems, the noise control effect here begins at the largest emission source, the wheels of the train. The absorbers are available in a walkable and drivable design and can be used both for, new construction and restoration. Poreton is a weather-resistant single-grain concrete, specially developed for track absorbers. It offers maximum resistance against mechanic influences and damage. Over hundreds of tracks have been equipped with the Rieton system by the company.

One of the top players in Fiber cement market, Equitone, have mastered themselves in façade materials over a period of time. The company’s facade materials can be attached to the building structure using a number of face and back fixing options. The facade panels are assembled on a vertical support structure that consist of metal profiles or wooden battens. Face fixing options include riveting and screwing on metal or wood supporting frames whereas, back fixing options are bonding or mechanical fixing on metal frames.

Equitone facade materials are assembled using the ventilated facade (rainscreen) system. The panels use open joints that add visual depth and allow for maximum back ventilation of the facade system. The rainscreen system creates healthy and safe buildings. Heavy downpour is kept outside the structure, yet it allows water vapor from inside the structure to escape.

James Hardie, an Australian based organization have created a good solution for houses. They introduced HardieShingle sidings and HardieTrim boards which give the distinct and elegant look to the houses. Shingles are a timeless design element. They enhance a home’s architectural features or as siding for a whole house, they embody classic beauty. As per the company, The HardieTrim boards complement the Hardie siding by offering long lasting protection and adds natural and beautiful look to the buildings.

American Fiber Cement Corporation has come up with Cembrit Patina board which is a strong, weather resistant cladding board characterized by its muted, matte finish. During manufacturing, the through-colored board receives a unique surface treatment which makes it powerfully resistant towards water staining and dirt, ensuring a long-lasting and durable facade. The natural credibility of the Cembrit is expressed through the slight color variations in the surface, imbuing the facade with the play of light and subtle difference associated with any natural building material. Over time, these natural variations may develop further as the surface patinates. The applications include Window reveals, Façade cladding, Internal Wall Linings, Balcony Panels and others.

The Switzerland based organization called Swiss Pearl are proactive in Fiber Cement market by creating vast design possibilities and outstanding product features of the products inspiring a young, creative design, as well as a practically oriented interior architecture. The spectrum of truly unique designs for living reaches today from the perfectly shaped outdoor furniture system via one-of-a-kind designs in seating groups, on to tables, shelves, lamps and more. The various end user objects include Birdy Nistbox, Dune Lounge, Ecal chair, Guhl desk, Mold lamp, Sponeck chair, Tetris shelf, Trash Cube stool and many more.

The companies referred to in the Fiber Cement Market research report includes Rieder Smart Elements GmbH, Equitone, James Hardie, Allura, American Fiber Cement, Fry Reglet, Swiss Pearl, Nichiha USA and more than 20 companies. Among all the above mentioned fiber cement market trends one more manufacturing carried out by major companies are coming up with the eco-friendly products in construction that will be fiber cement market growth.

What is our report scope?

The report incorporates in-depth assessment of the competitive landscape, product market sizing, product benchmarking, market trends, product developments, financial analysis, strategic analysis and so on to gauge the impact forces and potential opportunities of the market. Apart from this the report also includes a study of major developments in the market such as product launches, agreements, acquisitions, collaborations, mergers and so on to comprehend the prevailing market dynamics at present and its impact during the forecast period 2018-2024. All our reports are customizable to your company needs to a certain extent, we do provide 20 free consulting hours along with purchase of each report, and this will allow you to request any additional data to customize the report to your needs.

Key Takeaways from this Report

Evaluate market potential through analyzing growth rates (CAGR %), Volume (Units) and Value ($M) data given at country level – for product types, end use applications and by different industry verticals.

Understand the different dynamics influencing the market – key driving factors, challenges and hidden opportunities.

Get in-depth insights on your competitor performance – market shares, strategies, financial benchmarking, product benchmarking, SWOT and more.

Analyze the sales and distribution channels across key geographies to improve top-line revenues.

Understand the industry supply chain with a deep-dive on the value augmentation at each step, in order to optimize value and bring efficiencies in your processes.

Get a quick outlook on the market entropy – M&A’s, deals, partnerships, product launches of all key players for the past 4 years.

Evaluate the supply-demand gaps, import-export statistics and regulatory landscape for more than top 20 countries globally for the market.

Buy Now For more Chemicals and Materials related reports, please click here

The market for Europe LMS is forecast to reach $714.26 million by 2025, growing at a CAGR of 17.07% from 2020 to 2025. The market growth of Europe LMS is mainly attributed to the growing adoption of the elearning in training the employees. The growing government initiatives for the improvisation of digitalization is further impacting on the growth of the market.Report CoverageThe report: “Europe LMS Market – Forecast (2020-2025)”, by IndustryARC covers an in-depth analysis of the following segments of the Europe LMS market. By Module type: Collaborative Learning, Content Management, Talent Management, Performace Management, Assessment and Training, OthersBy End User: Information Technology, Healthcare, Biopharma, Transport, Retail, Food and Beverage, Hospitality, Manufacturing, Government and Defense, Telecom, OthersBy Geography: U.K, Germany, France, Italy, Spain, Netherlands, Belgium, Austria, Poland, Others

Key Takeaways

Retail is analysed to hold the highest share in the market owing to the growing adoption of eLearning in the training of the frontline workers market.

Germany region is expected to dominate the Europe LMS market during the forecast period 2020-2025 due to high investments in the connectivity solutions in the region.

The growing investments in the connectivity solutions such as 5G and IoT in Europe area is analysed to drive the market during the forecast period 2020-2025.

Europe LMS Market Segment Analysis – By module type

Europe LMS is segmented into collaborative learning, content management, talent management, performance management, assessment, testing and others. Collaborative learning is analysed to grow at highest rate during the forecast period 2020-2025 mainly attributed to the adoption of the gamified learning in the process. Adding to this, the growing automation and adoption of digitalization in almost every industry all over European countries is significantly contributing to the growth of the Europe LMS frontline workers training market.

Europe LMS Market Segment Analysis – By End user

Retail holds the highest market share of Europe LMS market in 2018, however, the transport segment is analysed to grow at highest rate during the forecast period. As the employees in transport industry are frequently on the move, LMS is a dire requirement for their training needs thereby significantly impacting on the growth of the Europe LMS frontline workers training market. Adding to this, the growing penetration of the digital technologies in training of the employees is set to boost the market growth rate. In April 2019, Virgin trains of UK Virgin Trains has partnered with students to help develop virtual reality technology to aid training in health and safety for new recruits. These initiatives are further impacting on the growth of the market during the forecast period 2020-2025.

Europe LMS Market Segment Analysis – By Geography

Germany is analysed to hold the highest market share in 2018. As the country is a major hub for transportation, manufacturing, and so on, the significant growth and adoption of digitalization in these industries in training the packers, drivers, pickers and others through the LMS system is set to contribute to the growth of the market during the forecast period 2020-2025. The significant rise in the investments in the expansions of the biopharma plants alongside the growing digitalization in the industry is set to boost the market for LMS. In June 2018, Boehringer Ingelheim has announced a 230 million euro investment into a new Biologicals Development Center (BDC) at the company’s research and development site thereby impacting on the growth of the market. The growing investments in the expansion of the manufacturing sector are set to further impact on the growth of the market.

Europe LMS market Drivers

Impact of global pandemic

The global pandemic COVID-19 has impacted on the adoption of the digital learning technologies for the employees. The significant number of cases in Europe region has resulted in the countries lockdown which created a dire need in employment of the LMS in training newly recruited employees thereby impacting on the growth of the market.

Europe LMS market Challenges

High Cost required for LMS Subscription

The high Cost required for learning platform Subscription, especially for enterprises with huge work force is limiting their adoption. The average cost required for Subscription of LMS Platforms is more than $30 per user per month and the annual licensing fees can be more than 20–25 percent of the initial cost. As huge number of frontline workforce are present in industries such as Manufacturing, Healthcare and Retail sector, so these higher subscription cost becomes an increasing burden for the industries. These industries are thus preferring to utilize non-tool based training, particularly OTJ training in its stead thus limiting the LMS adoption. Hence these high cost subscriptions effect the market growth in the forecast period 2020-2025.

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Europe LMS market. Europe LMS driver market is expected to be dominated by major companies such as Adobe, Blackboard, Canvas, Crossknowledge, Eurekos, Growth Engineering, Kallidus, Kenexa, Oracle, SAP among others.

Acquisitions/Technology Launches/Partnerships

In September 2018, Blackboard has launched Rebrand of Open-Source Learning Management System.

In January 2016, IBM Kenexa Learning Management System (LMS) on Cloud V5.0 enhancements can help organizations rapidly develop, deploy, and increase learner skills and capabilities.

For more Education related reports, please click here

Cloud management platform Market size was valued at $8.16 billion in 2019, and it is estimated to grow at a CAGR of 15.32% during 2020-2025. The growing trend for Bring Your Own Device (BYOD), and shifting focus toward cloud from on-premises have been providing opportunities for cloud management platform market. Rapid adoption of cloud based platform by IT enterprises and other organizations for improved operational efficiency set to drive the market. Furthermore, the dependence on cloud based solutions across various industry verticals has significantly increased the adoption of cloud platform for faster and customized services. This has been pushing the organizations to invest in cloud platform and this is anticipated to propel the Cloud management platform market growth during the forecast period.Key Takeaways

North America dominated the Cloud management platform market in 2019 owing to early adoption of advanced technologies and high investments in adopting them.

Growing demand for BYOD devices has been driving the market growth in IT companies and other organizations for high productivity of work in shorter period of time by reducing downtime errors.

Growing trend for digitalization has been pushing enterprises in adopting cloud based platform for maximum flexibility, reducing costs, increase the business agility, and to increase revenue.

The major drawback is the security concerns and lack of skilled expertise for solving the issues hinders the growth of the Cloud management platform market.

Deployment Mode – Segment AnalysisHybrid Cloud management platform segment held the largest share 39.56% in the Cloud management platform market in 2019. As hybrid cloud is the combination of both private and public cloud, many companies prefer this deployment mode for greater flexibility, and reliability. It enables organizations in connecting existing systems that run on traditional architectures. It offers benefits such as optimized cost management, improved analytics and increased efficiency. Adoption of this mode of deployment by IT organizations set to propel the cloud management market. Industry Vertical – Segment AnalysisBFSI sector is the fastest growing industry in cloud management platform market estimated to grow at a CAGR of 16.45%. The cloud platform provides banks the ability of responding quickly to the changes in the market with its scalability. It also assists BFSI sector to cope up with the changing needs of the customer and the technology to perform the tasks efficiently. It creates a multi channel relationship with the customers at every aspect of the service. It ensures banks and financial institutions in securing transactions and enhances better customer relationship. Online fund transfers, securing online payments, payment gateways, digital wallets, online fund transfer, and secure online payments can be done easily with the adoption of this platform. In January 2020, Temenos, the banking software company had partnered with Google cloud in order to assist financial organizations. This partnership has been made for smooth running of banking applications on Google Cloud that create profitable business models, and to improve customer experience. This is poised to drive the cloud management platform market in the BFSI sector in near future. Geography- Segment AnalysisNorth America dominated the Cloud management platform market in 2019 with a share of 38.56%, followed by Europe and APAC. As the North American countries such as the U.S. and Canada are the early adoption of advanced technologies, there is huge adoption of cloud management platform which is set to drive the market. Most of the key vendors such as Microsoft, VMware, IBM, Cisco, Hewlett Packard Enterprise, Oracle, CA Technologies and other companies have headquarters at U.S. Many U.S. companies have been acquiring other cloud management platform business to strengthen their businesses. For instance, at the end of 2018, Flexera had acquired one of the top multi cloud management provider RightScale to empower its IT services. These are the key factors for the growth of Cloud management platform market in North America.

Increased mobility and growing trend of bring your own device

Growing trend for Bring your own device (BYOD) in organizations and IT companies has driving the adoption of cloud platform. Cloud management platform can leverage and provides IT companies in controlling each and every system in the organization. The BYOD trend also drive organizations in adopting cloud based platform services for mobile device management mainly in the small and medium based enterprises where they lack the staff and budget in order to adequately deal. Cloud based platform provides most cost effective and least resource intensive way in order to secure data in the period of BYOD. It also helps IT employees to work anywhere and this set to increase the demand for cloud management platform market.

Increased savings and workforce productivity

With increasing digitalization, there has been significant shift towards adoption of cloud based platform. This platform provides greater flexibility and can be able to adopt and deploy services easily and monitor workloads which provide huge gain for the organization. According to Forbes survey, 64% of the respondents indicated that cloud-based collaboration tools have helped their organizations in executing work faster than before. Around 87% of the respondents indicated that cloud-based solutions represent a true breakthrough in collaboration. Additionally, cloud management platform provide consistency, reliability, increase scalability, accelerate workflows, and reduce disaster recovery downtimes to organizations and this set to escalate the market growth. Challenges – Cloud management platform Market

Complexity in designing the network for cloud and security concerns

High security issues and distributed denial of service attacks are the major challenges for cloud management platform. The lack of visibility pushes public security cloud and can lead to unauthorized access to data, improper handling, and duplication of data leading to the deletion of confidential data from infrastructure. In addition to these, the designing of networks from on-premises to cloud needs high investment which is one of the major challenges mainly for small medium enterprises that have small budgets. Complexity in designing of cloud platform is hindering the growth of the cloud management platform market. Market LandscapeAcquisitions and R&D activities are key strategies adopted by players in the cloud management platform market. In 2019, the market of Cloud management platform has been consolidated by the top ten players – Vmware, Microsoft, IBM, Cisco, Hewlett Packard Enterprise, Oracle, Dynatrace, CA Technologies, Micro Focus, Red Hat and others. Buy Now Acquisitions/Technology Launches

In August 2018, VMware had acquired Cloud Health Technologies Company which is a multi-cloud management platform that works on various platforms such as Goggle Cloud, Microsoft Azure, and AWS. VMware acquired this company in order to expand and manage public and private clouds that help customers in managing across a hybrid and multi cloud environment.

In February 2019, Microsoft had acquired DataSense Company for data management platform that can be used to collect, integrate and report information from online educational technology BrightBytes. Microsoft had integrated this functionality into Azure cloud platform to strengthen its portfolio. Thus, the acquisitions of the companies in order to expand the cloud platform services set to propel the cloud management platform market.

For more Information and Communications Technology related reports, please click here

The Hyper Automation Market is forecast to reach $200m by 2025, growing at a CAGR of 14% in the period 2019-2025. Hyper automation is the advancement of traditional automation capabilities by using technologies like artificial intelligence (AI), machine learning (ML) and other with robotic process automation(RPA) to automate processes. Banking financial services and insurance (BFSI) sector are going to play major role in growth of hyper automation and this technology is estimated to have highest adoption in banking financial services and insurance (BFSI) sector as most of the BFSI sector is using RPA which is estimated to be replaced by hyper automation. In manufacturing sector automobile industry is increasingly adopting hyper automation to verify the components that will need a warranty or replacement.Key Takeaways

Robotic process automation is main tool of hyper automation market which is going to be advanced by the use artificial intelligence, analytics and other. This technology development is driving the hyperautomation market

Hyper automation is estimated to have huge growth in Banking, financial services and insurance (BFSI) sector as the ability to perform many tasks such as data analyzing, data processing and others without any human intervention is driving the adoption.

Hyper automation is increasingly introduced as technological advancements have triggered businesses to overcome new challenges aimed to cope with changing consumer demand and requirements.

North America region dominated hyper automation market due to their demand in high precision applications and applications in Banking, financial services and insurance (BFSI)

Tool – Segment AnalysisThe tools required for hyper-automation are robotic automatic process (RPA), artificial intelligence, intelligent business management, analytics and other advanced tools, among the above robotic automatic process (RPA) is the core and expands automation capability with artificial intelligence (AI), process mining, analytics, and other advanced tools. The growth of hyper automation market is mainly driven by the ease in business processes with the installation of robotic process automation with artificial intelligence (AI), with the addition of many new features such intelligent business process management software (iBPM), natural language processing (NLP), analytics and other. Application – Segment AnalysisHyper automation is estimated to have great success in the banking, insurance and financial services sectors as hyper-automation can provide centralized updated data instantly. Hyper-automation improves accuracy and enables chief financial officers (CFO) to have live-data reporting, to reporting risk and enable fast decision using most current data. In manufacturing sector, automobile industry can use hyper automation to verify the components that may need a warranty or replacement. This growing set of applications is set to drive the hyper automation market demand led by BFSI segment which is estimated to grow at 19% CAGR through 2025. Geography – Segment AnalysisThe hyper automation market for North America held the largest market size in 2019 at 39% and is expected to dominate the market during forecasted period. U.S. is the largest market for Banking, financial services and insurance (BFSI) and most of the tasks such as customer service, accounts payable, mortgage processing and others are operated using robotic process automation (RPA). Now with introduction of many advance tools such as artificial intelligence (AI), process mining, analytics, and others with robotic process automation (RPA), hyper automation or advanced robotic automation process can perform many task such as data analyzing, data processing and others without any human intervention. Thus, many regions such as Canada, Mexico and others which have large BFSI sectors using robotic process automation (RPA) are going to be huge market for hyper-automation. Drivers – Hyper Automation Market

Increasing penetration of automation

Technological advancements have triggered businesses to overcome new challenges aimed to cope with changing consumer demand and requirements. In recent years, the adoption of automation has captured the attention of many small, medium and large sized enterprises as automation has many benefits such as increase in employee capacity, greater productivity and accurate insights and others which are leading to increase in penetration of automation. Hyper-automation has many benefits such as reduction in errors, reduction in work time for humans and improvement in quality of work. Thus this market is set to witness significant rise in market penetration

Surge in demand for precision and accuracy in various industry verticals-

Accuracy plays a major part in data extraction process, and human beings have issues in providing accurate data. Thus, as hyper automation provides accurate data through the use of data mining, machine learning and other processes, this technology is set to witness increased adoption. Data extraction and data accuracy plays a major role in analytics; hyper automation uses extracted data for analyzing and automating the whole process by using robotic process automation. With the use of advanced tools such as artificial intelligence, machine learning and others, hyper automation can not only reduce the risk of human error but also human effort and thus will witness significant rise in adoption.

As technology is getting updated day-by- day, it is not possible for the many industries to provide proper training to the employees, which is leading to delay in implementation of new technology in various industries. Without being aware of where automation is required in business and following the trend blindly, implementing it would be a disaster. Training plays the major role in implementing advance tools such as artificial intelligence, machine learning, natural language processing and other. However the lack of training among employees provides a major hindrance in the adoption of hyper automation. Market Landscape The key players in the field of hyper automation market are Google, Amazon, Uipath, Blueprism, automation anywhere, AutomationEdge and others Partnerships/Product Launches/Acquisition

In February 2020, Automation Anywhere, announced the world’s first integrated artificial intelligence (AI)-driven process discovery solution that discovers business processes to be operated by bots

In March 2020,CogniBot a Hyper automation platform with next generation AI capabilities is launched Automation Edge which is going to help the business user to record their actions and development using tools like drag and drop .

For more Information and Communications Technology related reports, please click here

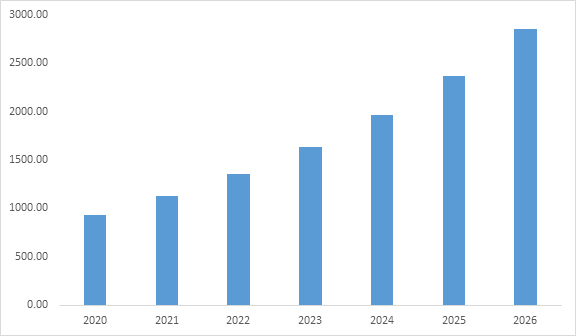

Board Portal market size is expected to reach $2849.7 million by 2026 at a CAGR of 17.0% during the forecast period 2021-2026. A board portal is a system that secures and completes works based on internet technology that will be used to facilitate management meetings, communication and collaboration between directors and the board of directors. In addition it is used for providing content to the directors either on mobile devices or on different websites. As cybercrime is increasing rapidly, the demand for a secure meeting platform for boards has been increasing widely.

Moreover board portal software offers the highest level of security as it uses highest grade of encryption and security applications for limited access to documents, chats and confidential mails. Further, companies are increasingly showing interest in meeting management software as it has taken everything from paper-based formats to all digital board materials planning, delivery and retrieval. Hence these factors enhances the adoption of Board Portal Software market in the forecast period 2021-2026.

The report: “Board Portal Industry Outlook – Forecast (2021-2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Board Portal market By Type: Enterprise Model/Onsite, Hosted/Client Hosted, Vendor Hosted/SaaS, Others (Third Party Hosted) By Deployment: Cloud, On Premise By End Use Industry: Oil and Energy, Education, BFSI, Healthcare, Government and Public Service, Law Firms, Media and Entertainment, ISP/Telecom, Others By Organization Size: SME, Large Enterprises By Geography: North America (U.S, Canada, Mexico), Europe(Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, SK, Aus and Others), South America(Brazil, Argentina and others), and RoW (Middle East and Africa)

Key Takeaways

Board Portal software in North America is growing at significant rate owing to early adoption of advanced technologies and rising adoption of smart technologies has been driving the board portal in this region.

The global demand for board software has been rising rapidly over the last few years due to the high adoption of cloud-based technology integration with the portal software of the enterprise, which enables companies to operate their own applications on cloud platforms.

Vendor Hosted/Software as a Service (SaaS) is growing at a highest CAGR of 19.4% in the forecast period. This SaaS Model has gained popularity among various end-user segments and is expected to maintain substantial market share in the forecast period.

Board Portal top 10 companies include NASDAQ, Computershare, Diligent, Azeus Convene, Visma/AdminControl., Aprio Inc., Passageways, BoardPaq LLC., Directorpoint LLC, and Modevity LLC among others.

Vendor Hosted/SaaS is growing at a highest CAGR of 19.4% in the forecast period. This SaaS Model has gained popularity among various end-user segments and is expected to maintain substantial market share in the forecast period as a result of higher model security measures and lower initial and continuing costs incurred by customers. In addition, SaaS solutions also allow companies to generate industry-specific customer data and intelligence. The growth of SaaS models contributes to making board portal software more accessible. Meeting Management Software is implemented either by IT or subscription-based software as a service (SaaS).

With the cost reduction of on-demand computing power, a substantial increase in Internet accessibility and the rise of smartphone and tablet device vendors, several businesses will offer portal services at lower cost and in a more open manner. Moreover this model has gained traction between different end-user segments and is expected to hold considerable market share in the forecast period as a result of higher platform security measures and lower initial and continuing costs for customers. SaaS solutions also help businesses to generate customer data and information that is specific to each industry. Board Portal Software is easy to use, easily scalable and less prone to data loss favours an agile development life cycle and these are forcing the demand for SaaS model in the forecast period 2020-2025.

Board Portal Market Segment Analysis – By End User

Healthcare sector for this board meeting management software market is growing at a CAGR of 22.6% in the forecast period. Rising adoption of board portals in hospitals is an intuitive step and with the ability to have tremendous paper and printing savings, productivity increases for administrative staff who streamline distribution of materials, savings in binding and delivery of printed materials, information security, convenient board access anywhere with an internet connection and streamlined distribution of changed and added materials hospitals are preferring board portal.

Many of the issues facing hospital boards today include high board numbers, demands for financial management, the need for well-informed board members and continuing education. In these rapidly changing times, the hospital board of directors needs board portal software to dramatically streamline governance, share information and interact effectively. The 2018 Health Leaders Media Industry Survey found that while 69 per cent of hospital executives said their boards were strong or very strong, 11 per cent said their boards were weak or bad. This is also attributed to the large number of members of the hospital board of directors.

The answer to this perplexing compromise is the incorporation of portal tools from the hospital board. The board portal software is designed for the collaboration of hospital boards with a single shared interface for all board documents and activities and is therefore expected to fuel the market growth of Board Portal. Further using board portals for healthcare organizations, such as BoardBookit, can allow those brave, creative, flexible leaders to thrive in a changing environment. Moreover the decision to integrate board portals for pharmaceutical companies that will adapt and change as quickly as the pharmaceutical market is necessary, critical, and fundamental to modern board procedures.

Board Portal Market Segment Analysis – By Geography

Board Portal in North America is growing at significant rate of 15.9% owing to early adoption of advanced technologies and rising adoption of smart technologies in this country has been driving the board portal in this region. In addition several benefits offered by board portals, help organizations in different ways mainly through prepare and distribute files effortlessly, make pre-meeting annotations, to access documents anywhere, to allow seamless real-time collaboration, and enhance corporate social responsibility. Moreover features of board meeting management software are always up to date, easy to use, industry leading security, e-signature, two way authentication, attendance tracker and among others.

Further cloud-based business end-users in this region are experiencing a large-scale adoption of advanced technology and telecommunications in the region. Furthermore, the involvement of the region’s major players based on new product launches is expected to infuse tremendous market growth. In 2019, Passageways, a global provider of secure, intuitive collaboration solutions, released third-generation OnBoard board portal software platform which is explicitly engineered to improve meeting outcomes for organizations of all sizes. Hence growing developments as such drive the market growth in the forecast period 2021-2026.

Board Portal Market Drivers

High adoption of cloud-based technologies integration with the organization’s portal services:

The global demand for board portal software has been rising rapidly over the last few years due to the high adoption of cloud-based technology integration with the portal services of the enterprise, which enables companies to operate their own applications on cloud platforms. In addition cloud-based board portals provide a more effective use of time and resources due to the availability of information on a common platform. Moreover rising need to strengthen security standards for confidential documents in most organizations driving the market growth. Further board meeting management software offers access to information and data to the right people and prohibits access to unauthorized persons.

In emerging cloud-based services, business information is stored online, resulting in a rapid increase in cloud-related cyber-attacks, which, in turn, increase the demand for stable and reliable software, such as board portal software: stimulating market growth. With the rising penetration of the Internet across the globe and the growing need for remote employees to understand the business process at ground level, BYOD programs have become crucial to the technical landscape. As a result, BYOD has emerged as a catalyst to enable the company to prioritize the efficiency of its employees without compromising protection. Hence these factors drive the growth of board portal in the forecast period 2021-2026.

Adoption of board portal software in healthcare industry:

Many of the issues facing hospital boards today include high board numbers, demands for financial management, the need for well-informed board members, and continuing education. In these rapidly changing times, the hospital board of directors needs board portal software to dramatically streamline governance, share information and interact effectively. For instance according to the report given by health leaders in 2018, more than 69 per cent of hospital executives said their boards were strong or very strong, 11 per cent said their boards were weak or bad.

This is also attributed to the large number of members of the board of directors of hospitals. The solution to this perplexing compromise is the incorporation of portal tools from the hospital board. In the middle, the software hits the boards and their members by increasing contact. Moreover board portal software is optimized for the collaboration of hospital boards with a single shared interface in the meeting management software for all board documents and activities and is therefore expected to fuel Board Portal’s market growth.

Board Portal Market Challenges

Initial expense and lack of unskilled workforce:

The installation costs of board portals are relatively higher. Thus, many organizations still prepare board materials in big paper packets and mail them prior to each meeting. In future, awareness about the software and its potential applications may likely fuel the market growth of board portals in respective end user industries. Board portals are used in wide range of verticals which includes financial services, education, healthcare, oil & energy and others. However, limited awareness on the security and reliability of these services in oil & gas and some other end users pose challenge board portals adoption in market. Moreover, data security and privacy concerns associated with utilization of meeting management software are also an acting as hindrance for these services.

Software launches, acquisitions, Expansions, Partnerships and R&D activities are key strategies adopted by players in the Board Portal software market. In 2020, the market of Board Portal industry outlook has been fragmented by several companies. Board Portal top 10 companies include NASDAQ, Computershare, Diligent, Azeus Convene, Visma/AdminControl., Aprio Inc., Passageways, BoardPaq LLC., Directorpoint LLC, and Modevity LLC among others.

Acquisitions/Technology Launches

In 2020, Diligent Corporation entered into a partnership with Heidrick & Struggles and Egon Zehnder, a joining founding partner of Spencer Stuart. These partnership aimed to posting open board opportunities specifically for diverse candidates within the Diligent Director Network to enhance their Modern Leadership initiative.

For more Information and Communications Technology related reports, please click here